-

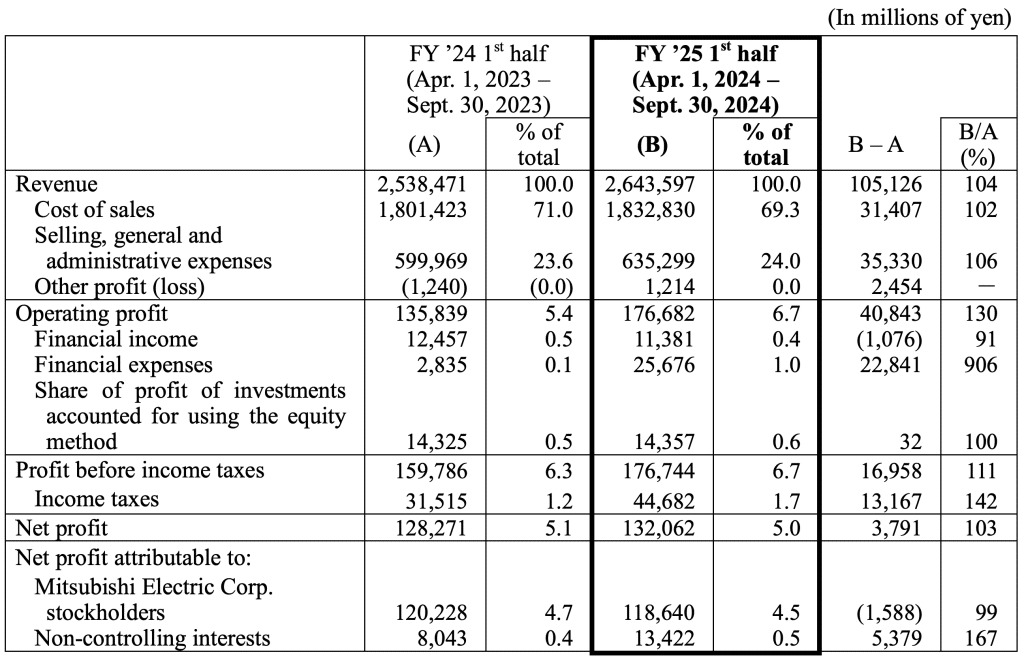

Mitsubishi Electric Corporation announced its consolidated financial results for the second quarter (first half), ended September 30, 2024, of the current fiscal year ending March 31, 2025 (fiscal 2025).

Original – Mitsubishi Electric

-

Qorvo® announced financial results for the Company’s fiscal 2025 second quarter ended September 28, 2024.

On a GAAP basis, revenue for Qorvo’s fiscal 2025 second quarter was $1.047 billion, gross margin was 42.6%, operating income was $9.7 million, and loss per share was $0.18. On a non-GAAP basis, gross margin was 47.0%, operating income was $212.2 million, and diluted earnings per share was $1.88.

Bob Bruggeworth, president and chief executive officer of Qorvo, said, “In the September quarter, ACG successfully supported our largest customer’s seasonal smartphone ramp. In HPA, we expanded our D&A business while building a broad-based business in power management. In CSG, we maintained our leadership in Wi-Fi applications while investing to grow in diverse businesses including automotive solutions and SoCs for ultra-wideband and Matter. HPA and CSG are on pace to achieve mid-teen year-over-year growth in fiscal 2025.”

Grant Brown, chief financial officer of Qorvo, said, “In the September quarter, we exceeded the midpoint of guidance in revenue, gross margin and EPS. Looking forward, the flagship and premium tiers in the smartphone market are holding up well, however, content and ramp profiles vary by model, and we are experiencing unfavorable mix. We expect this to continue in the second half of fiscal 2025. In addition, in the mid and entry tiers of Android 5G smartphones, mix has shifted toward entry-tier 5G at the expense of mid-tier 5G. In our current view, we don’t expect this mix shift in Android 5G from mid-tier to entry-tier to reverse. As a result, we are taking appropriate actions, including factory consolidation and operating expense reductions as well as focusing on opportunities that align with our long-term profitability objectives. We currently expect full-year fiscal 2025 revenue and gross margin will be slightly down versus fiscal 2024.”

Qorvo’s current outlook for the December 2024 quarter is:

- Quarterly revenue of approximately $900 million, plus or minus $25 million

- Non-GAAP gross margin of approximately 45%

- Non-GAAP diluted earnings per share between $1.10 and $1.30

Original – Qorvo

-

Littelfuse, Inc. reported financial results for the third quarter ended September 28, 2024:

- Net sales of $567 million were down 7% versus the prior year period and organically

- GAAP diluted EPS was $2.32 and adjusted diluted EPS was $2.71

- Cash flow from operations was $80 million and free cash flow was $65 million

“In the third quarter, our global teams delivered strong execution and drove sales and earnings above our expectations,” said Dave Heinzmann, Littelfuse President and Chief Executive Officer. “While we see soft end market conditions extending into the fourth quarter, we remain focused on driving operational excellence while serving our global customer base and delivering meaningful new business wins. Our proven growth strategy, diversification efforts and strong technology capabilities position us to deliver top tier long-term stakeholder value.”

Based on current market conditions, for the fourth quarter the company expects Net sales in the range of $510 – $540 million, adjusted diluted EPS in the range of $1.90 – $2.10 and an adjusted effective tax rate of approximately 14%.

Original – Littelfuse

-

onsemi announced results for the third quarter of 2024 with the following highlights:

- Revenue of $1,761.9 million

- GAAP gross margin and non-GAAP gross margin of 45.4% and 45.5%, respectively

- GAAP operating margin and non-GAAP operating margin of 25.3% and 28.2%, respectively

- GAAP diluted earnings per share and non-GAAP diluted earnings per share of $0.93 and $0.99, respectively

- Returned 75% of free cash flow over the last 12 months to shareholders through stock repurchases

“With third-quarter results above expectations, we remain focused on delivering consistent results in the current environment through execution and prudent financial management,” said Hassane El-Khoury, president and CEO, onsemi.

“As power demands continue to rise across our key markets, and the need for greater efficiency becomes paramount, we are investing to win across the entire power spectrum to ensure that onsemi is best positioned to gain share in automotive, industrial and AI data center.”

Original – onsemi

-

As expected, the business performance of Siltronic AG in Q3 2024 was characterized by subdued demand from the semiconductor industry.

“In a persistently challenging market environment, we have delivered solid quarterly results. Consequently, we can confirm our guidance for the full year 2024. However, it remains uncertain when chip manufacturers’ inventories will return to normal levels,” commented Dr. Michael Heckmeier, CEO of Siltronic AG on the developments.

Siltronic generated sales of EUR 357.3 million in Q3 2024, an increase of 1.7 percent compared to the previous quarter (Q2 2024: EUR 351.3 million). This is due to an increase in wafer area sold, which was partially offset by opposing product mix effects. After nine months, the company reported sales of EUR 1,052.2 million, a decrease of 9.1 percent year-on-year (Q1-Q3 2023: EUR 1,157.2 million). This was mainly due to the lower wafer area sold. In addition, product mix-, price- and FX effects also had a slightly negative impact.

Cost of sales increased by 2.6 percent in Q3 2024 compared to the previous quarter, mainly due to higher wafer area sold and a moderate increase in depreciation. For the first nine months of 2024, cost of sales decreased by 2.5 percent compared to the same period in 2023. The disproportionate decline compared to sales is primarily due to a reduced dilution of fixed costs and higher depreciation.

As a result, the gross profit fell by EUR 1.4 million compared to the previous quarter and from January to September 2024 by EUR 83.1 million compared to the previous year. The gross margin fell from 25.3 percent to 20.0 percent year-on-year.

EBITDA in Q3 was EUR 89.4 million and thus on the level of the previous quarter (Q2 2024: EUR 90.6 million). The EBITDA margin remained at a solid level of 25.0 percent (Q2 2024: 25.8 percent). After nine months, Siltronic reported an EBITDA of EUR 270.7 million (Q1-Q3 2023: EUR 342.8 million) and an EBITDA margin of 25.7 percent (Q1-Q3 2023: 29.6 percent).

Due to the lower EBITDA and higher depreciation, EBIT amounted to EUR 28.9 million in Q3 (Q2 2024: EUR 33.0 million) and to EUR 97.8 million after the first nine months (Q1-Q3 2023: EUR 194.5 million). Net profit for the quarter was EUR 18.8 million (Q2 2024: EUR 22.4 million) and earnings per share were EUR 0.60 (Q2 2024: EUR 0.73). Net income for the period from January to September was EUR 68.8 million (Q1-Q3 2023: EUR 169.0 million) and earnings per share of EUR 2.19 after EUR 5.13 in the same period of the previous year.

With an equity ratio of 47.1 percent as of September 30, 2024 (December 31, 2023: 46.6 percent), Siltronic continues to maintain a good balance sheet quality. Loan liabilities increased mainly due to the partial draw of a loan. Additionally a promissory note loan was successfully placed in September and paid out in early October. At roughly EUR 370 million, the original issue volume was significantly exceeded.

“We are pleased with the high level of interest in this transaction. The strong demand is a demonstration of the promissory note loan investors’ trust in the company,” adds Claudia Schmitt, CFO of Siltronic AG.

Cash flow from operating activities for the period January to September 2024 decreased by EUR 83.3 million compared to the previous year. This was mainly due to the lower EBITDA and the change in prepayments. In the same period of the previous year, there was a significant net inflow, while in the first nine months of the financial year there was a net outflow of prepayments.

Despite a noticable reduction in capex during the year, cash outflows for capex remained at a high level of EUR 565.1 million, mainly due to the construction of the new 300 mm fab in Singapore. Accordingly, net cash flow, which excludes cash inflows and outflows from prepayments, was negative as expected at EUR -317.7 million (Q1-Q3 2023: EUR -631.3 million).

As a result, cash and cash equivalents and financial investments decreased by EUR 168.4 million to EUR 290.7 million in the first nine months of 2024. Siltronic thus reported net financial debt of EUR 739.1 million at the end of September 2024.

As already communicated in the half-year report 2024, Siltronic AG’s Executive Board expects sales to be in the high single-digit percentage range below the previous year. This is primarily due to the lower wafer area sold, as well as each slightly negative FX rate (EUR/USD 1.10), price- and product mix effects.

The customer qualifications that are decisive for the start of depreciation of the new fab in Singapore have been delayed from the fourth quarter of 2024 into next year. As a result, depreciation of the new fab and other ramp costs that impact earnings will occur over the course of 2025. Accordingly, the full-year EBITDA margin guidance is adjusted to 24 to 26 percent. Depreciation and amortization for 2024 will therefore be lower and is expected to be between EUR 230 million and EUR 250 million. Capex including intangible assets remains unchanged and will be in the range of EUR 500 million to EUR 530 million.

Despite the challenging market environment, the company anticipates a significant growth potential in the medium and long term. Key drivers of this growth are megatrends such as Artificial Intelligence, Digitization, and Electromobility. With its investments in expanding production capacity and improving the product mix, Siltronic is well-positioned to profitably support this growth.

Original – Siltronic

-

Texas Instruments Incorporated reported third quarter revenue of $4.15 billion, net income of $1.36 billion and earnings per share of $1.47. Earnings per share included a 3-cent benefit for items that were not in the company’s original guidance.

Regarding the company’s performance and returns to shareholders, Haviv Ilan, TI’s president and CEO, made the following comments:

- “Revenue decreased 8% from the same quarter a year ago and increased 9% sequentially. Industrial continued to decline sequentially, while all other end markets grew.

- “Our cash flow from operations of $6.2 billion for the trailing 12 months again underscored the strength of our business model, the quality of our product portfolio and the benefit of 300mm production. Free cash flow for the same period was $1.5 billion.

- “Over the past 12 months we invested $3.7 billion in R&D and SG&A, invested $4.8 billion in capital expenditures and returned $5.2 billion to owners.

- “TI’s fourth quarter outlook is for revenue in the range of $3.70 billion to $4.00 billion and earnings per share between $1.07 and $1.29. We continue to expect our fourth quarter effective tax rate to be about 13%.”

Original – Texas Instruments

-

Aehr Test Systems announced financial results for its first quarter of fiscal 2025 ended August 30, 2024.

Fiscal First Quarter Financial Results:

- Net revenue was $13.1 million, compared to $20.6 million in the first quarter of fiscal 2024.

- GAAP net income was $0.7 million, or $0.02 per diluted share, compared to GAAP net income of $4.7 million, or $0.16 per diluted share, in the first quarter of fiscal 2024.

- Non-GAAP net income, which excludes the impact of stock-based compensation, acquisition-related costs, and amortization of intangible assets, was $2.2 million, or $0.07 per diluted share, compared to non-GAAP net income of $5.2 million, or $0.18 per diluted share, in the first quarter of fiscal 2024.

- Bookings were $16.8 million for the quarter.

- Backlog as of August 30, 2024 was $16.6 million.

- Total cash, cash equivalents and restricted cash as of August 30, 2024 were $40.8 million, compared to $49.3 million at May 31, 2024, reflecting $10.6 million in net cash paid during the quarter for the acquisition of Incal Technology, Inc.

Gayn Erickson, President and CEO of Aehr Test Systems, commented:

“We finished the first quarter with revenue and non-GAAP net income ahead of consensus estimates and are off to a good start to our fiscal year. Silicon carbide wafer level burn-in test systems and full wafer contactors are poised to be key contributors to revenue again this year. We are also forecasting material bookings and revenue contributions from several other markets this fiscal year, as we are successfully executing on our strategy to expand our test and burn-in products into other large and fast-growing markets such as artificial intelligence processors, gallium nitride power semiconductors, hard disk drive components and flash memory devices.

“We have been seeing a stabilization and increasingly positive discussions within the silicon carbide power semiconductor market over the past quarter. Electric vehicle (EV) suppliers are clearly moving towards silicon carbide in integrated modules, combining silicon carbide MOSFETs into single packages to meet the industry’s power, efficiency, and cost-effectiveness demands. Due to the need for extensive test and burn-in of these devices to ensure reliability for mission-critical applications like EVs, the benefits of conducting this screening at the wafer level before integrating them into modules, which may sometimes contain 32 or more other devices, are becoming clear. The process improves yields and reduces costs, driving demand for wafer level burn-in, an area where Aehr Test stands as the low-cost leader and proven solution for this critical testing. We are highly optimistic about our silicon carbide business and expect it to gain momentum over the next few quarters. Our silicon carbide customers are forecasting capacity expansion needs in calendar 2025, with several anticipating purchases of one or two systems in early 2025, followed by production volumes in the second half of the year, and ramping further into 2026.

“Meanwhile, we continue to see strong demand for our FOX WaferPakTM full wafer Contactors for silicon carbide, driven by a record number of new device designs started this past quarter. These designs are expected to lead to additional WaferPak purchases for engineering qualification as well to volume production orders as they advance to production. We had another solid quarter for WaferPak sales, generating over $12 million in revenue from WaferPaks in the first quarter.

“We are also making steady progress on our previously announced benchmarks and engagements with new silicon carbide device and module suppliers. We are confident that we will add several new silicon carbide customers this year, establishing our solution as their tool of record for volume production. Additionally, silicon carbide is gaining traction in applications beyond electric vehicles, such as solar, industrial, and data centers, which will expand our addressable markets.

“We are now in negotiations with our first gallium nitride (GaN) semiconductor customer for volume production wafer level test and burn-in of their devices. This past year, this customer purchased a significant number of WaferPaks to successfully qualify a wide range of GaN device types aimed at multiple markets, including consumer, industrial, and automotive. In addition, we have had increased discussions and engagements with multiple potential new GaN suppliers. We believe GaN is a significant up and coming technology for power semiconductors. With a forecasted CAGR of more than 40% to over $2 billion in GaN devices sold annually by 2029, it has the potential to be a significant market opportunity for Aehr’s wafer level solutions.

“Last quarter, we announced that an Artificial Intelligence (AI) accelerator company committed to evaluating our FOXTM solution for wafer level burn-in of their high-power processors. This evaluation is underway at our Fremont facility, where multiple wafers are being tested using our proprietary WaferPaks and new high-power FOX-XP and NP systems, which provide up to 3500 watts of power delivery and thermal control per wafer. We are delivering over 2000 amperes of current to a single 300 mm wafer, allowing us to burn-in numerous processors with our proprietary test modes. The evaluation is progressing very well, and once we demonstrate successful wafer level test results and throughput, we anticipate they will adopt our high-power FOX-XP systems for production of their next-generation AI processors, beginning this fiscal year.

“During the quarter we announced and completed our acquisition of Incal Technology, Inc. We are excited to bring the combined strengths of both companies to market as we begin engaging with Incal’s customers, including many AI industry leaders. Customer feedback to this acquisition has been overwhelmingly positive, with several meetings held over the past few weeks where some customers indicated increased forecasts for engineering qualification as well as for volume production.

“Last month, we were pleased to announce the first volume production orders for Incal’s new Sonoma ultra-high-power semiconductor packaged part test and burn-in solution designed for AI accelerators, graphics processors, network processors, and high-performance computing processors. These orders were placed by a large-scale data center hyperscaler that provides computing power and storage capacity to millions of users worldwide. The integration with Incal is progressing well. We have already shipped several systems since the acquisition, and we plan to consolidate personnel and manufacturing into Aehr’s Fremont facility by the end of the fiscal year.

“Last quarter, we announced a key customer in the hard disk drive space that is now forecasting a production ramp-up starting this fiscal year for a new high-volume data storage device application. This customer is finalizing their capacity requirements, and we expect this ramp-up to drive orders for multiple FOX-CP production systems and WaferPak Contactors, with shipments likely occurring in the second half of this fiscal year. We see the data storage market, along with various devices supporting the global 5G expansion, as new growth opportunities for our systems, as these markets require devices with exceptionally high levels of quality and long-term reliability.

“With all of these customer engagements, market opportunities, and the products to address them, we are very optimistic about the year ahead, and we are reaffirming our financial guidance for revenue growth and profitability for the year.”

For the fiscal year ending May 30, 2025, Aehr is reiterating its previously provided guidance for total revenue of at least $70 million and net profit before taxes of at least 10% of revenue.

Original – Aehr Test Systems

-

Wolfspeed, Inc. announced its results for the fourth quarter of fiscal 2024 and the full 2024 fiscal year.

Quarterly Financial Highlights (Continuing operations only. All comparisons are to the fourth quarter of fiscal 2023.)

- Consolidated revenue of approximately $201 million, as compared to approximately $203 million

- Mohawk Valley Fab contributed approximately $41 million in revenue

- Power device design-ins of $2.0 billion

- Quarterly design-wins of $0.5 billion

- GAAP gross margin of 1%, compared to 29%

- Non-GAAP gross margin of 5%, compared to 31%

- GAAP and non-GAAP gross margins for the fourth quarter of fiscal 2024 include the impact of $24 million of underutilization costs. See “Start-up and Underutilization Costs” below for additional information.

Full Fiscal Year Financial Highlights (all comparisons are to fiscal 2023)

- Consolidated revenue of approximately $807 million, as compared to approximately $759 million

- GAAP gross margin of 10% as compared to 32%

- Non-GAAP gross margin of 13% as compared to 35%

- GAAP and non-GAAP gross margins for fiscal 2024 include the impact of approximately $124 million of underutilization costs. See “Start-up and Underutilization Costs” below for additional information.

“We have two priorities we are focused on: optimizing our capital structure for both the near term and long term and driving performance in our state-of-the-art, 200-millimeter fab, and this quarter was a step forward on both of these priorities,” said Wolfspeed CEO, Gregg Lowe.

“We achieved 20% utilization at Mohawk Valley in June and continued to see strong revenue growth from that fab. Our 200mm device fab is currently producing solid results, which are at significantly lower costs than our Durham 150mm fab. This improved profitability gives us the confidence to accelerate the shift of our device fabrication to Mohawk Valley, while we assess the timing of the closure of our 150mm device fab in Durham. At the JP, we have also made great progress, installing and activating initial furnaces in the fourth quarter. We have already processed the first silicon carbide boules from the JP and the quality is in line with the high-quality materials coming out of Building 10.

“At the same time, we are taking proactive steps to slow down the pace of our CapEx by approximately $200 million in fiscal 2025 and identify areas across our entire footprint to reduce operating costs. We also remain in constructive talks with the CHIPS office on a Preliminary Memorandum of Terms for capital grants under the CHIPS Act. In addition to any potential capital grants from the CHIPS program, our long-term CapEx plan is expected to generate more than $1 billion in cash refunds from Section 48D tax credits from the IRS, of which we’ve already accrued approximately $640 million on our balance sheet,” continued Lowe.

Business Outlook:

For its first quarter of fiscal 2025, Wolfspeed targets revenue from continuing operations in a range of $185 million to $215 million. GAAP net loss is targeted at $226 million to $194 million, or $1.79 to $1.54 per diluted share. Non-GAAP net loss from continuing operations is targeted to be in a range of $138 million to $114 million, or $1.09 to $0.90 per diluted share.

Targeted non-GAAP net loss excludes $88 million to $80 million of estimated expenses, net of tax, primarily related to stockbased compensation expense, amortization of discount and debt issuance costs, net of capitalized interest, project, transformation and transaction costs and loss on Wafer Supply Agreement.

The GAAP and non-GAAP targets from continuing operations do not include any estimated change in the fair value of the shares of common stock of MACOM Technology Solutions Holdings, Inc. (MACOM) that we acquired in connection with the sale to MACOM of our RF product line (RF Business Divestiture).

Start-up and Underutilization Costs:

As part of expanding its production footprint to support expected growth, Wolfspeed is incurring significant factory start-up costs relating to facilities the Company is constructing or expanding that have not yet started revenue generating production. These factory start-up costs have been and will be expensed as operating expenses in the statement of operations.

When a new facility begins revenue generating production, the operating costs of that facility that were previously expensed as start-up costs are instead primarily reflected as part of the cost of production within the cost of revenue, net line item in our statement of operations. For example, the Mohawk Valley Fab began revenue generating production at the end of fiscal 2023 and the costs of operating this facility in fiscal 2024 and going forward are primarily reflected in cost of revenue, net.

During the period when production begins, but before the facility is at its expected utilization level, Wolfspeed expects some of the costs to operate the facility will not be absorbed into the cost of inventory. The costs incurred to operate the facility in excess of the costs absorbed into inventory are referred to as underutilization costs and are expensed as incurred to cost of revenue, net. These costs are expected to continue to be substantial as Wolfspeed ramps up the facility to the expected or normal utilization level.

Wolfspeed incurred $20.5 million of factory start-up costs and $24.0 million of underutilization costs in the fourth quarter of fiscal 2024. No underutilization costs were incurred in the fourth quarter of fiscal 2023.

For the first quarter of fiscal 2025, operating expenses are expected to include approximately $25 million of factory start-up costs primarily in connection with materials expansion efforts. Cost of revenue, net, is expected to include approximately $24 million of underutilization costs in connection with the Mohawk Valley Fab.

Original – Wolfspeed

- Consolidated revenue of approximately $201 million, as compared to approximately $203 million

-

Analog Devices, Inc. announced financial results for its fiscal third quarter 2024, which ended August 3, 2024.

“ADI’s revenue finished above our guided midpoint with stronger profitability driving earnings per share near the high end of our outlook,” said Vincent Roche, CEO and Chair. “As we navigate this business cycle’s nascent recovery, our high-performance analog solutions portfolio positions us well to intersect the strong underlying stream of concurrent secular trends. Our innovation and customer-centric ethos will continue to form the foundation for our success and help drive long-term shareholder value.”

“Improved customer inventory levels and order momentum, across most of our markets, position us to grow again sequentially in our fourth quarter, increasing our confidence that we are past the trough of this cycle. However, economic and geopolitical uncertainty continues to limit the pace of the recovery” said Richard Puccio, CFO.

Performance for the Third Quarter of Fiscal 2024 (PDF)

Outlook for the Fourth Quarter of Fiscal Year 2024

For the fourth quarter of fiscal 2024, we are forecasting revenue of $2.40 billion, +/- $100 million. At the midpoint of this revenue outlook, we expect reported operating margin of approximately 22.3%, +/-180 bps, and adjusted operating margin of approximately 41.0%, +/-100 bps. We are planning for reported EPS to be $0.85, +/-$0.10, and adjusted EPS to be $1.63, +/-$0.10.

Our fourth quarter fiscal 2024 outlook is based on current expectations and actual results may differ materially as a result of, among other things, the important factors discussed at the end of this release. These statements supersede all prior statements regarding our business outlook set forth in prior ADI news releases, and ADI disclaims any obligation to update these forward-looking statements.

The adjusted results and adjusted anticipated results above are financial measures presented on a non-GAAP basis. Reconciliations of these non-GAAP financial measures to their most directly comparable GAAP financial measures are provided in the financial tables included in this release. See also the “Non-GAAP Financial Information” section for additional information.

Dividend Payment

The ADI Board of Directors has declared a quarterly cash dividend of $0.92 per outstanding share of common stock. The dividend will be paid on September 17, 2024 to all shareholders of record at the close of business on September 3, 2024.

Original – Analog Devices

-

Ideal Power Inc. reported results for its second quarter ended June 30, 2024.

“Our B-TRAN™ commercial progress continued with several significant developments over the last three months. We are now collaborating with a third global automaker and achieved two more of our 2024 milestones with the addition of a second global distributor and the qualification of a second high volume production fab. We are pleased to see multiple large companies in our test and evaluation program advancing to place initial orders,” said Dan Brdar, President and Chief Executive Officer of Ideal Power. “We remain on track to achieve our 2024 milestones and look forward to more commercial announcements in the coming months.”

Key Second Quarter and Recent Business Highlights

Execution to our B-TRAN™ commercial roadmap continues, including:

- Collaborating with a third global automaker. This auto OEM is evaluating B-TRAN™-enabled contactors as a potential replacement for electromechanical contactors in its electric vehicles.

- Finalizing a distribution agreement with a second global distributor with particular strength in Asia. This distributor is already placing orders with us.

- Qualified a second wafer fabrication supplier with high-volume production capability. With the addition of this European partner, we are dual sourced for wafer fabrication in different parts of the world with ample capacity to support anticipated customer demand over the next few years.

- Secured orders for B-TRAN™ devices and circuit breaker evaluation boards from a global leader in power semiconductor and power electronics solutions in connection with its launch of a multi-year DC power distribution system program. This global leader presents multiple opportunities for us as it addresses several of our target industrial markets: solid-state circuit breakers (“SSCB”) for industrial facilities and electric utility grid infrastructure and renewable energy.

- Secured an order for B-TRAN™ devices for evaluation in solar inverter applications from a top 10 global provider of power conversion solutions to the solar industry. This customer is a previously announced participant in our B-TRAN™ test and evaluation program.

- Secured an order for SymCool® power modules and drivers from a Forbes Global 500 power management market leader initially in our B-TRAN™ test and evaluation program. This global power management market leader is evaluating SymCool® against IGBT modules for use in SSCB applications.

- Added a global leader in circuit protection, industrial fuses and power conversion technology with over a billion in annual sales to the roster of the B-TRAN™ test and evaluation program.

- Based on the results of testing, we increased the current rating of our SymCool® power module from 160A to 200A, a 25% increase. In conjunction with a power module size reduction of approximately 50%, this results in a dramatic increase in power density for the SymCool® power module.

- B-TRAN™ Patent Estate: Currently at 87 issued B-TRAN™ patents with 40 of those issued outside of the United States and 45 pending B-TRAN™ patents. Current geographic coverage includes North America, China, Japan, South Korea, India, and Europe, with pending coverage in Taiwan.

Second Quarter 2024 Financial Results

- Cash used in operating and investing activities in the second quarter of 2024 was $2.2 million compared to $1.8 million in the second quarter of 2023.

- Cash used in operating and investing and activities in the first half of 2024 was $4.2 million compared to $3.7 million in the first half of 2023.

- Raised $15.7 million in net proceeds from a public offering. Received net proceeds of $13.7 million upon initial closing in March 2024 followed by net proceeds of $2.0 million from the exercise of the underwriter’s overallotment option in April 2024.

- Cash and cash equivalents totaled $20.1 million at June 30, 2024.

- No long-term debt was outstanding at June 30, 2024.

- Commercial revenue was $1,331 in the second quarter of 2024.

- Operating expenses in the second quarter of 2024 were $2.9 million compared to $2.4 million in the second quarter of 2023 driven primarily by higher research and development spending.

- Net loss in the second quarter of 2024 was $2.7 million compared to $2.3 million in the second quarter of 2023.

2024 Milestones

For 2024, the Company has set or achieved the following milestones:

√ Successfully completed Phase II of development program with Stellantis

• Secure Phase III of development program with Stellantis

√ Complete qualification of second high-volume production fab

• Convert large OEMs in our test and evaluation program to design wins/custom development agreements

√ Add distributors for SymCool® products

• Initial sales of SymCool® IQ intelligent power module

• Begin third-party automotive qualification testingOriginal – Ideal Power